How to Dispute Business Credit Report Errors

Your business credit report is one of the most critical financial documents you’ll encounter as a small business owner. Lenders, suppliers, and creditors use it to evaluate your creditworthiness when you apply for SBA loans, vendor credit lines, or equipment financing. Unfortunately, errors on your business credit report are more common than you might think—and they can cost you thousands of dollars in higher interest rates or denied funding requests.

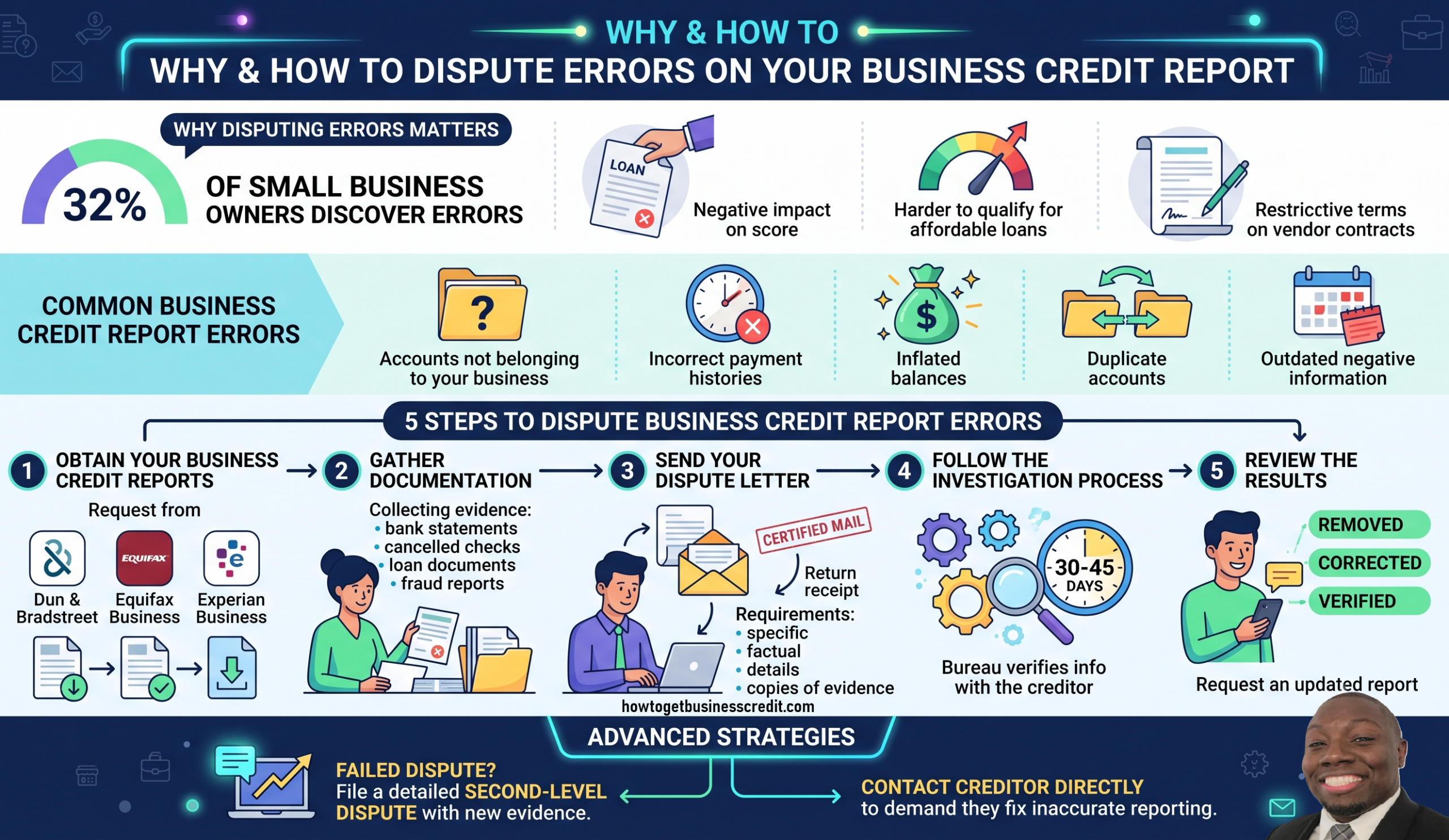

According to the National Small Business Association, approximately 32% of small business owners discover errors on their business credit reports. These mistakes can range from accounts you don’t recognize to incorrect payment histories or outdated negative information. The good news? You have legal rights to dispute these errors and get them corrected.

This comprehensive guide will walk you through the entire process of disputing business credit report errors, protecting your access to affordable capital, and ensuring your financial reputation accurately reflects your business practices.

Understanding Business Credit Report Errors

Common Types of Errors

Business credit errors fall into several categories, each requiring different dispute strategies. Understanding which type of error you’re facing helps you build a stronger dispute case and increases your chances of successful resolution.

Account Errors: The most common mistake is accounts listed that don’t belong to your business. This might include accounts opened by someone using your EIN fraudulently, merged accounts from previous business structures, or accounts from another business with a similar name. These errors are particularly damaging because they suggest you have obligations you’ve never actually incurred.

Payment History Errors: Incorrect payment status notations are surprisingly frequent. You might see accounts marked as 30, 60, or 90 days late when you actually paid on time, or accounts showing as delinquent when you’ve maintained a current status. These errors directly impact your credit score and your ability to qualify for SBA loans with favorable terms.

Balance Errors: Sometimes credit bureaus report incorrect outstanding balances on active accounts. This inflates your debt-to-income ratio and makes you appear riskier to lenders than you actually are. If you’re seeking a $250,000 SBA 7(a) loan, an inflated balance of even $50,000 could affect your approval odds.

Duplicate Accounts: Your business might appear to have the same account listed multiple times, which artificially increases your reported debt and creates confusion about your actual credit obligations.

Outdated Information: Negative information like charge-offs, collections, or late payments should eventually fall off your report. Federal law requires derogatory items to be removed after 7 years from the original delinquency date. If you’re seeing older negative marks, those are errors you can successfully dispute.

Why These Errors Matter

Business credit errors directly impact your ability to access affordable capital. An error that lowers your business credit score by 50 points could increase your SBA loan interest rate by 1-2%, meaning you’d pay tens of thousands in additional interest over a 10-year repayment period on a $500,000 loan.

Beyond loan rates, these errors affect your ability to:

- Establish vendor credit lines that don’t require upfront payment

- Negotiate better payment terms with suppliers

- Qualify for equipment leasing or financing

- Secure commercial insurance at competitive rates

- Attract potential business partners or investors

Step-by-Step Guide to Disputing Business Credit Report Errors

Step 1: Obtain Your Business Credit Report

Before you can dispute errors, you need to see what’s being reported about your business. Unlike personal credit, there’s no single “free” business credit report you’re entitled to annually. However, the major business credit bureaus—Dun & Bradstreet, Equifax Business, and Experian Business—all provide access to your business credit reports, typically for a fee of $20-$75 per report.

Glen Gould recommends requesting reports from all three bureaus, as they often have different information. An error on one bureau’s report might not appear on another’s, so checking all three ensures you catch everything.

When you receive your reports, review them carefully for:

- Incorrect business name, address, or phone number

- Wrong EIN or tax ID number

- Accounts you don’t recognize

- Inaccurate payment histories

- Incorrect balance amounts

- Information that should have been removed (older than 7 years)

Step 2: Gather Documentation

Your dispute will be much more effective when you include supporting evidence. Strong documentation dramatically increases the likelihood of successful resolution. Collect the following materials:

For Payment Disputes: Bank statements showing the payment was made, cancelled checks, payment receipts from the creditor, or ACH transfer confirmations. Keep these organized chronologically to show your payment pattern.

For Account Disputes: Original credit applications (or their absence if you never applied), correspondence with the creditor, and any fraud reports you’ve filed with law enforcement or the Federal Trade Commission.

For Balance Disputes: Recent statements from the actual creditor showing your current balance, loan documents showing the original loan amount, and payment records demonstrating how much you’ve paid down.

For Duplicate Accounts: Account numbers from your statements, any correspondence from the creditor about account consolidation, and documentation showing these are the same obligation.

Step 3: Send Your Dispute Letter

Federal law (the Fair Credit Reporting Act) requires you to send your dispute in writing. While phone calls or online disputes might be available, a written letter creates a paper trail and ensures your dispute is documented.

Your dispute letter should:

- Be Specific: Don’t just say “this is wrong.” Clearly state what information is inaccurate and what the correct information should be.

- Include Your Business Information: Your business name, EIN, phone number, and the address on file

- Reference the Disputed Account: Include the account number or creditor name from the credit report

- Request Verification: Ask the bureau to verify the information with the reporting creditor and remove it if it cannot be verified

- Be Professional: Keep emotions out of the letter and stick to facts

- Include Copies (Not Originals): Attach copies of your supporting documentation

- Request Confirmation: Ask the bureau to send you written confirmation once the dispute is resolved

Send your letter via certified mail with return receipt requested to:

- Dun & Bradstreet: Disputes Department, 103 JWL Drive, Wilmington, DE 19801

- Equifax Business: Equifax Business Disputes, P.O. Box 740256, Atlanta, GA 30374

- Experian Business: Experian Business Disputes, P.O. Box 9701, Allen, TX 75013

Step 4: Follow the Investigation Process

Once the credit bureau receives your dispute, they have 30-45 days to investigate. During this period, they contact the creditor reporting the information and ask them to verify its accuracy. If the creditor cannot verify the information within the timeframe, the bureau must remove it.

Many disputes are resolved successfully during this period simply because creditors don’t respond to verification requests quickly or at all. This is where having detailed documentation becomes crucial—creditors are more likely to respond when a bureau inquiry comes with your supporting evidence attached.

Step 5: Review the Results

The credit bureau will send you written results of their investigation. They might:

- Remove the Information: The best outcome—the error is deleted from your report entirely

- Correct the Information: The item stays but with accurate details (different balance, correct payment status, etc.)

- Verify the Information: The bureau confirms the information is accurate. If you disagree, you can request a second-level dispute

If the dispute is resolved in your favor, ask the bureau to send an updated copy of your credit report and provide copies to any creditors who received the inaccurate information in the past 6 months.

Advanced Dispute Strategies for Persistent Errors

Second-Level Disputes

If the bureau’s initial investigation doesn’t resolve the issue or you disagree with their findings, you have the right to file a second-level dispute. This is particularly useful when:

- The creditor verifies information you believe is incorrect

- You have additional documentation you didn’t include in the first dispute

- The bureau failed to investigate thoroughly

Your second-level dispute should be more detailed, highlighting specifically why you believe the bureau’s investigation was inadequate and including any new evidence.

Direct Creditor Disputes

While disputing with the credit bureau is important, also dispute directly with the creditor reporting the error. Send them a certified letter explaining the inaccuracy and requesting they contact the credit bureau to correct or remove the information. Some creditors respond faster to direct contact than they do to bureau verification requests.

Working with Funding-Advisor.com for Complex Cases

For disputes involving fraud, identity theft, or particularly damaging errors, consider getting professional assistance. Funding-Advisor.com can help you navigate complex disputes and ensure your business credit is restored to where it should be, making you more competitive for SBA loans and other capital.

Protecting Your Business Credit Going Forward

Monitor Regularly

Don’t wait years to discover errors. Check your business credit reports at least annually—more frequently if you’ve had disputes in the past. Many business credit bureaus offer affordable monitoring services that alert you to changes.

Maintain Documentation

Keep copies of all business credit applications, statements, payment confirmations, and correspondence with creditors for at least 7 years. This documentation makes future disputes much easier to resolve.

Optimize Your Business Credit Profile

Beyond disputing errors, actively improve your business credit by:

- Paying all invoices on time

- Maintaining low credit utilization (ideally below 30%)

- Keeping business credit accounts open even when inactive

- Regularly reviewing your business credit reports

How Corrected Business Credit Impacts Your Funding

Correcting errors on your business credit report can have dramatic effects on your access to capital. Consider this example: a business with a credit score of 60 would struggle to qualify for an SBA loan. If that low score was due to an error that you successfully dispute, your score might jump to 75-80, making you eligible for SBA 7(a) loans up to $5 million with rates typically ranging from 7-10% depending on your term length and down payment.

For a $250,000 SBA loan over 10 years, the difference between a 9% and 11% interest rate (potentially caused by the credit error) is approximately $24,000 in additional interest paid. Disputing the error not only fixes your reputation—it saves you significant money.

Frequently Asked Questions

Q: How long does a business credit dispute take?

A: The initial investigation period is 30-45 days from when the credit bureau receives your dispute. However, actual resolution can take 60-90 days depending on how quickly creditors respond to verification requests and whether you need to file second-level disputes.

Q: Can I dispute business credit errors online?

A: While some credit bureaus offer online dispute tools, sending a written certified letter is more effective and creates better documentation. Consider using both methods to maximize your chances of resolution.

Q: What if the creditor won’t remove the error?

A: If you believe a creditor is deliberately reporting false information, you can file a complaint with the Consumer Financial Protection Bureau (CFPB) or your state’s attorney general office. You also have the right to add a statement to your credit report explaining the dispute.

Q: Does disputing hurt my business credit score?

A: No, disputing an error does not hurt your credit score. The dispute inquiry itself is not reported to other creditors and does not trigger a hard inquiry that affects your score.

Q: How can I get a loan while disputing errors?

A: You can apply for SBA loans during the dispute process, though approval might be delayed until the dispute is resolved. Lenders often wait for resolution of significant disputes before finalizing funding. Disclose the dispute in your loan application to maintain transparency with lenders.

Get Expert Business Funding Guidance

Book Free Strategy Call or call 850-990-0053